The Future of Payments: LFG’s Role in Simplifying Transactions

The Hangover

Do you remember the collective hallucination that was "DeFi Summer."?

If you look back, it wasn't a 'pure' financial revolution like the advertising said. Yes some amazing work was done by some truly tallented people that led the way to even more innovation now. But also, it was Spring Break for degens.

It was an orgy of leverage, flaunting reckless bets, and anonymous founders playing blackjack with other people's life savings.

Then came the crash.

The False Knight

The crisis was on the cards, the industry looked for a savior. Changpeng Zhao (CZ) of Binance rode in on a white horse, but he wasn't there to save the patient, FTX.

He pulled the rug, exposed the rot, and watched his biggest rival burn. It was Machiavellian brilliance. But it revealed a terrifying truth. If it could happen to Sam Bankman-Fried, the media darling and effective altruist, could it happen to anyone. Coinbase, Binance, Kraken?

If your money is on a company's balance sheet, it is not your money. It is an unsecured loan to a CEO who might be insane.

This remains true today, which is madness.

If you park your funds on a major crypto exchange, there is no FDIC insurance to save you. If they fall, you lose everything.

This is not the case with non-custodial wallets like LFG. We don't hold your money, you do.

The Flight to Safety

Predictably, trust in centralized exchanges plummeted. The refugees fled to non-custodial wallets.

After the dust settled, the conversation returned. Suddenly everyone, your mom, your dad, your neighbor, even your grandma, was back in the game. The consensus was absolute: Non-custodial was the only way. "Not Your Keys, Not Your Crypto" became the new gospel.

But the refugees ran into a new problem. The technology sucked.

The existing non-custodial wallets were built by engineers, for engineers. The dashboards looked like the control panel of a Soviet moon lander. To send a transaction, you needed a PhD in cryptography and a Xanax.

Worse, these wallets were "blind." They had no checks, no balances, and no compliance. They were perfect for keeping your money safe from SBF, but useless for doing business in the real world.

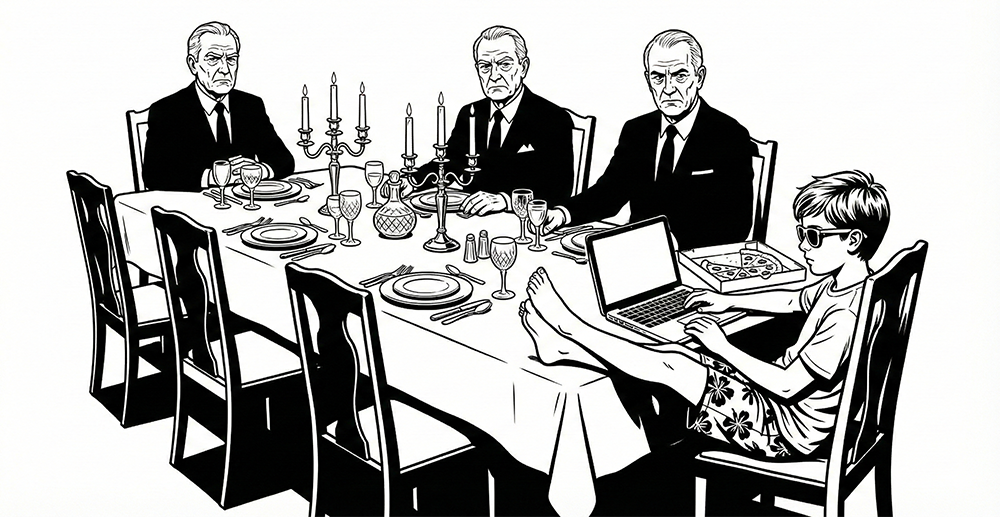

The Dinner Table Problem

Here is the uncomfortable truth. If you want to build a real business, you have to interact with the incumbents. You need to connect with banks, payment processors, and tax authorities.

To do that, you have to sit nicely at the dinner table.

You cannot show up to a meeting with JP Morgan with your feet on the table, wearing board shorts, passing anonymous funds to "CryptoGod69." The banks will not just kick you out. They will debank you and lock the door.

Case in Point: The JP Morgan Freeze

We watched this play out in real time. JP Morgan froze the accounts of two Y-Combinator backed stablecoin startups, Blindpay and Kontigo.

The crypto Twitter echo chamber immediately cried foul. They screamed that this was an anti-competitor move or an anti-crypto crusade by the big bad banks.

It wasn't.

The reality is far more embarrassing. These startups did not even hold institutional accounts at the bank. They accessed banking services via an intermediary called Checkbook. When JP Morgan detected high-risk flows, allegedly involving sanctioned jurisdictions like Venezuela, they didn't just flag a transaction; they cut off the access point.

Regulation is not the enemy. Identity confusion is.

It is amazing how "crypto is hard" usually means someone onboarded sanctioned users, cosplayed as a bank, then acted surprised when the actual bank noticed. If you interface with regulated finance, you inherit regulated standards.

Even less sympathy is deserved when your website pretends to be a bank, then quietly walks it back in the footnotes. Regulators notice that. Banks definitely do.

This is not anti-crypto. It is anti-pretending.

...But the party is over, and now the lights are on, the music has stopped, and the headache is blinding.

Now comes the hard part: The clean-up.

While the rest of the industry is still stumbling around looking for the next dopamine hit, we are focused on the one thing that actually matters: Sobriety.

The Designated Driver

We believe the blockchain is the greatest settlement layer ever invented. It is faster than Visa and cheaper than a wire transfer. But it has a fatal flaw: It was hijacked by gamblers.

You cannot build a serious business on a currency that moves like a meme stock. If your accounts receivable fluctuates by 20% between the invoice date and the payment date, you don't have a business. You have a casino.

At LFG, we act as the designated driver. We strip away the speculation. We settle exclusively in USDC.

Why USDC? Because in a post-hangover world, you want water and aspirin, not moonshine. Tether (USDT) operates in the shadows; USDC is the audited, regulated, fully-backed adult in the room. We don't take risks with your runway.

The Crypto STD

Volatility isn't the only thing you catch in the unregulated wild west. There is something worse.

In DeFi, anonymity is treated as a feature. In business, it is a bug. When you accept a payment from a random hexadecimal wallet address (0x4f3...), you have no idea where that money has been.

If that wallet interacted with a sanctioned entity, or even if it interacted with someone who interacted with a sanctioned entity five transactions ago, that money is tainted.

We call this The Crypto STD.

It is silent, invisible, and highly contagious. You might have sold a perfectly legal coffee, but if the coin you received has a dirty history, the banking system will treat you like a money launderer. They will freeze your accounts, and they won't tell you why.

Financial Hygiene

LFG is the prophylactic layer for your revenue.

We introduced Pre-Compliance, a concept that shouldn't be revolutionary, yet somehow is.

Verified Profiles: No more anonymous strings of code. You transact with verified businesses.

The firewall: We scan every single transaction before it settles. We check the chain history five transactions back and five transactions forward.

If the money is dirty, the transaction is declined before it happens. We block the infection at the door so you never have to explain yourself to a regulator or bank.

The Cure

The killer app of blockchain isn't 10,000% APY. It isn't a picture of a monkey.

The killer app is moving value around the world instantly, for near-zero cost, without asking a bank or Crypto exchange for permission.

We built LFG to preserve that utility while filtering out the toxicity. We give you the tech without the noise, the rails without the risk, and the speed without the hangover.

Time to sober up.

The Adult in the Room

We built LFG because we refused to accept that binary.

We believe you should hold your own funds. We never touch your money. We are non-custodial by design. That protects you from us.

But we also believe that "non-custodial" shouldn't mean "non-compliant." We built a UI that your CFO can actually understand. More importantly, we built the compliance layer. These are the checks and balances that allow you to take your crypto wealth and sit at the dinner table with the legacy financial system.

Some of us solved the "risk" problem in the product design phase.

We are not here to kill the banks. We are here to help you transact with them without handing over the keys to your vault.

The party is over. It’s time to get to work,

Kris

Kris Krogh

Written by Kris Krogh, a payments and fintech expert with a passion for simplifying global transactions

You Might Also Like

Check out more posts that explore the future of payments and fintech solutions